The SBA 7(a) loan is one of the most popular business loan options, providing a range of great benefits for your business. As with many business loans, when you apply for a 7(a) loan you may be required to pledge collateral. Depending on the size of the loan and your available business assets, you may be required to pledge your home or investment property as collateral.

This overview of the SBA 7(a) collateral requirements will help you understand what may be required as collateral when you apply for this loan program. With this information, you’ll be able to better determine the best option for your business.

What are SBA 7(a) and Community Advantage loans?

SBA 7(a) loans are a terrific option for growing businesses. It’s the U.S. Small Business Administration’s (SBA) most popular loan option because it offers easier approval criteria, terms that make repayment easier, and a range of approved uses, providing borrowers with a lot of flexibility. Explore why an SBA 7(a) loan could be the best choice for your first business loan.

SBA Community Advantage loans are a type of 7(a) loan that provides funding for businesses in underserved geographic areas. SBA 7(a) loans are available from $50,000 to $5 million, and Community Advantage offers loans up to $350,000.

What types of real estate factor into SBA loans?

There are three different types of real estate that you’ll hear about when it comes to SBA loans and collateral requirements, including:

- Project real estate: This is where your business currently operates from (or will operate from once the project is complete) and is almost always improved commercial real estate, but can also be vacant land.

- Residential real estate: This can include primary residences or residential rental properties that are owned.

- Investment real estate: This can be owned personally, by a business or by a trust and is improved commercial real estate.

What are the collateral requirements for SBA 7(a) and Community Advantage loans?

If your business already owns enough equipment, inventory, furnishings, and other assets to meet the SBA 7(a) collateral requirements, then the SBA considers the loan “fully secured.” When calculating this, the SBA looks at the adjusted net book value of the assets, including:

- Improved real estate, which can be valued at a maximum of 85% of market value. This can include SBA project real estate, residential real estate, or other investment real estate.

- Unimproved real estate, which can be valued at 50% of the market value. This typically refers to any vacant residential or investment real estate that’s owned, but could potentially include SBA project real estate that will remain as vacant land.

- New machinery and equipment (besides furniture and fixtures), valued up to 75% of the price, less any previous liens.

- Used or existing machinery and equipment (excluding furniture and fixtures), up to 50% of net book value (or up to 80% with an orderly liquidation appraisal), less prior liens.

- Furniture and fixtures up to 10% of the net book value or appraised value.

- Lenders may also include trading assets (inventory and accounts receivable) valued at a maximum of 10% of the current book value.

What if your business doesn’t meet the SBA 7(a) collateral requirements?

In many cases, businesses won’t have enough collateral for the SBA to consider the loan “fully secured.” If you find yourself in this situation, you may need to take a lien against your residential and investment real estate. The SBA may also require this for any owners who own 20% or more of your business, or any additional required personal guarantors.

It’s important to know that if you have less than 25% equity in the real estate, the SBA typically won’t require that it be pledged as collateral on the loan.

Additionally, if you can put more funds into the project and reduce the amount borrowed to meet the “fully secured” definition, then you may not be required to use residential and investment real estate as collateral.

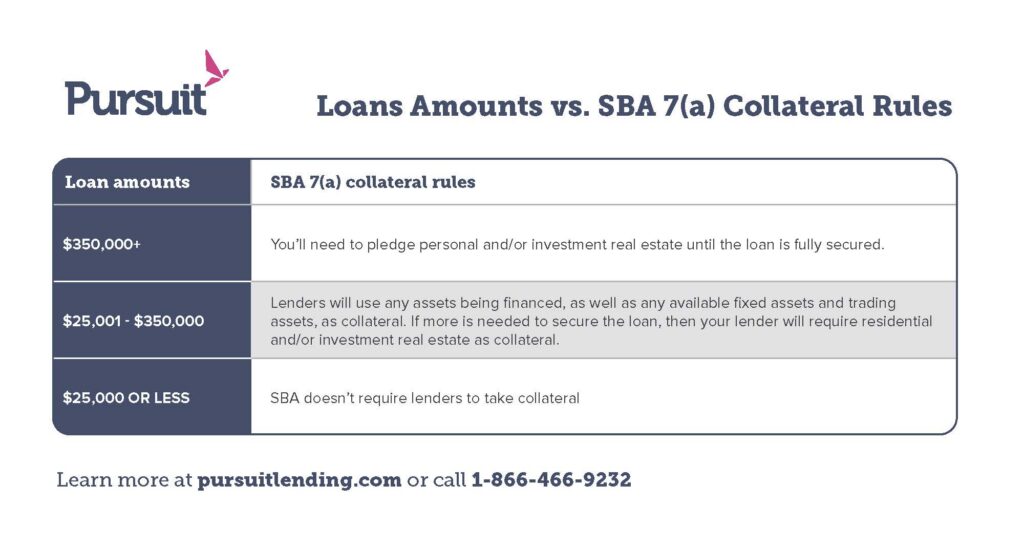

Important exceptions for SBA 7(a) loans of $350,000 or less

There are exceptions to the SBA 7(a) collateral requirements on loans that are less than $350,000, including all Community Advantage loans:

- For loans of $25,000 or less, the SBA doesn’t require lenders to take any collateral.

- For loans between $25,001 and $350,000, lenders will do the following:

- They’ll first use any assets that are being financed by the loan as well as any available fixed assets and trading assets as collateral.

If those assets don’t fully secure the loan, then the loan will require residential and/or investment real estate as collateral.

When is it required for residential or investment real estate to be used as collateral?

If the loan amount you’re requesting is above $350,000, you’ll need to include personal residential and/or investment real estate as collateral. However, you’ll only need to pledge collateral to the point where there’s no longer a shortfall and the loan is “fully secured.” Here are a few items to note:

- The SBA doesn’t require lenders to collateralize loans with personal real estate (residential and investment) to meet the “fully secured” definition when the equity in the real estate is less than 25% of the property’s fair market value. In these cases, lenders must document the source (other than personal financial statements) in their loan files to make these determinations. Gain clarity on SBA 7(a) loan equity requirements and how to properly document your equity.

- Liens on residential and investment real estate may be limited to 150% of the equity in the collateral by the lender, if there are tax implications associated with the lien amount in the state where the lien is filed.

- Certain states don’t permit primary residences to be pledged as collateral on business loans. Depending on the state where you reside, your home may not be available as collateral.

When will I know if I’ll be required to pledge personal real estate?

When you apply for an SBA 7(a) or Community Advantage loan, your lender will draft a transaction structure that includes an estimate of any collateral shortfall. This is the first step in determining the estimated gap to meet the SBA’s “fully secured” definition.

Your lender will then evaluate available collateral and determine whether any additional properties must be pledged.

With this information, your lender will also review the “soft costs,” such as title insurance and searches, recording fees, and any mortgage recording tax that will be required, and will talk with you about what may be needed to close your loan.

Some additional important FAQs

Here are some of the frequently asked questions and concerns about the SBA 7(a) collateral requirements:

Q: My real estate is held by an entity – does this exclude it from being able to be pledged?

A: Not necessarily. If you own the majority of the entity or the entity is solely owned by you (or you and your spouse jointly), then it’s not excluded from your available collateral. This includes any real estate (residential or investment) that’s owned by personal trusts.

Q: My spouse solely owns the property – does this exclude it from being able to be pledged?

A: Yes, as long as your spouse isn’t required as a guarantor. They could be required as a guarantor if they have an ownership interest of 20% or more in the business. This also applies if there’s a combined ownership interest between the spouses or minor children of 20% or more. If your spouse is a required guarantor, the property is considered part of your available collateral.

If your spouse is not a required guarantor, then the property would not typically be required as part of the collateral unless the timing of the ownership change was done in close proximity to the SBA application.

Q: My estimated value of the property provides insignificant equity when mortgage or HELOC balances are considered. Does this exclude it from being able to be pledged?

A: Yes and no. The SBA requires residential or investment property collateral if the available equity (defined as “asset value less existing mortgage and /or HELOC liabilities”) is more than 25% of the value of the property.

However, you can’t determine the value in your personal financial statement. It must be documented by another source, as determined by your lender.

Q: The costs to record the mortgage and obtain title insurance are very expensive. Does this exclude it from being able to be pledged?

A: No, however, the SBA may allow a mortgage lien to be limited to 150% of the available equity in the residential or investment property if there are costly tax implications with recording the mortgage.

Q: Does the mortgage have to be in the full amount of the loan?

A: Yes, however, in some cases, the mortgage lien can be limited to the amount of the collateral shortfall or 150% of the available equity in the residential or investment property (not project property) if there are costly tax implications with recording the mortgage.

Q: I own multiple properties, including my home and some investment properties. Can I specify which property is offered for collateral?

A: Yes, in some cases, the SBA allows borrowers to specify a preference for which properties are used as collateral. However, the final decision will be made by your lender based on credit risk and their credit policy.

Q: Can my real estate be released before the loan is paid in full?

A: This decision will ultimately be up to your lender, but the SBA is aware of situations that may arise during the life of the loan that will require collateral changes. For example, if you move and sell your home, the SBA or your lender will require that the lien be placed on the new home and will have processes in place to swap the collateral.

Whatever your needs, Pursuit can help

Whether you need financing for buying a business, commercial real estate, or construction and improvements, the SBA 7(a) loan program can be a great option – and Pursuit can be the lender that helps bring your vision to life.

Every day, we help small business owners like you navigate the SBA 7(a) loan process – and a range of other business loans and a line of credit – to help you secure the funds you need to launch and grow.

Contact us today to learn more about the ways we can help!