Imagine you’ve found the perfect location for your new business and suppliers whose goods will thrill your customers when they walk through the door. You’ve applied for the financing you need, too, and you’re so close to bringing this all to fruition – but if the requirements for a startup business loan aren’t fulfilled accurately and on time, it could delay your funds and derail your plans.

With the five tips in this article, you’ll learn how to satisfy key requirements for a startup business loan and avoid common delays so your business is ready to launch or grow.

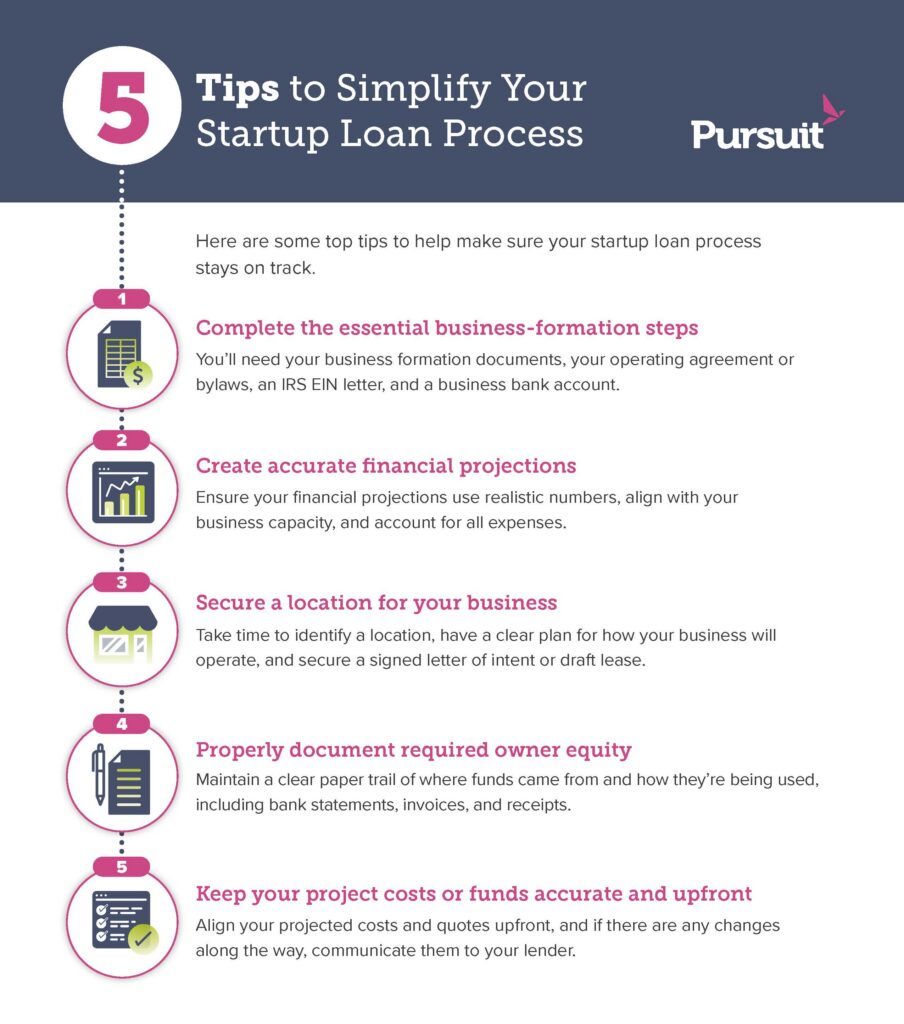

5 tips to simplify your startup loan process

Getting a small business loan is a big step for you and your business, but if there are hiccups in the funding process, it can be frustrating and slow things down.

The good news is that most loan delays come from a small number of avoidable issues:

1. Complete the essential business-formation steps

If you haven’t completed key steps in the business-formation process, you won’t be eligible for small business funding.

Before you apply for a small business loan, be sure that your business is fully formed and ready to verify. Experts at your local or regional Small Business Development Center (SBDC) or SCORE can help you develop a business plan and financial projections, and an accountant or a small business attorney can help with business formation.

Before starting the loan process, you’ll need to have key documents available, including:

- Your business’s formation documents (such as an LLC or corporation registered with your state, or—if you’re a sole proprietor—a DBA (“doing business as”) registration if you’re using a business name instead of your personal name

- Your operating agreement (for LLCS) or bylaws (for corporations), which outline how your business is structured and run

- An SS-4 (EIN letter) from the IRS to show that you’ve received an Employer Identification Number (EIN)

- A business bank account to keep your business and personal finances separate

2. Create accurate financial projections

Your lender will review the assumptions behind the financial projections detailed in your business plan to determine if your business will generate enough cash flow to support loan repayment. If the numbers aren’t supported or appear overly optimistic, it may raise “red flags” for the lender and cause delays.

For example, if your plan for your auto-repair shop includes two bays and two part-time technicians and it’s open eight hours a day, four days a week, then revenue that depends on repairing 80 cars a week may or may not be realistic. Similarly, if your projections don’t account for all operating expenses – such as payroll, rent, or marketing – these gaps will be identified during review.

For your financial projections, you’ll want to:

- Align your revenue with your business’s actual capacity

- Reflect a realistic ramp-up for growth

- Fully account for all expenses

- Ground your numbers in how the business will truly operate

The experts at SBDCs and SCORE can help you create realistic and achievable projections. This will give you peace of mind while avoiding common pitfalls – and it demonstrates to your lender that you’ve invested time and effort and are willing to learn from experts.

3. Secure a location for your business

A business’s location is a key part of the loan review process. If a location hasn’t been identified or changes during underwriting or closing, it can delay the process or, in some cases, result in the application being withdrawn or re-evaluated.

It’s important that you:

- Take the time to identify the right location for your business

- Have a clear plan in place for how your business will operate

- Secure a signed letter of intent (LOI) or a draft lease outlining the proposed space

If, during the loan process, a better opportunity comes up or your plans change, communicate with your lender as soon as possible so they can assess any impact and keep the process moving.

4. Properly document required owner equity

Most responsible small business loans require an owner equity contribution – and when it isn’t properly documented, it’s the most common cause of delays. Cash or unexplained deposits typically won’t qualify, and if the source and use of funds can’t be clearly verified, the application will stall.

Lenders will want to see:

- A clear paper trail showing where funds came from, that they’ve been seasoned (meaning they’ve been in your account long enough to verify the source), and how they were used

- If funds have already been spent, they must tie directly to project costs and be supported by documentation such as bank statements, invoices, and receipts

Maintaining clear financial records helps lenders verify the source and availability of funds for your project and can help prevent delays during underwriting or loan closing. Without proper documentation, the funds generally can’t count toward equity.

5. Keep your project costs or funds accurate and upfront

A small business loan is approved based on a specific set of costs and uses of funds. If those numbers change – whether due to updated quotes, cost increases, or shifts in how funds are allocated – it can impact the structure of the loan and may require the deal to be re-evaluated.

For example, if you were approved based on a certain amount for equipment and working capital, but updated quotes come in significantly higher, or funds need to be reallocated, those changes can delay the process while underwriting reassesses the project scope.

Be sure that:

- Your projected costs and quotes are as accurate and aligned as possible upfront

- You communicate any changes to your lender immediately so they can evaluate the impact and help keep things moving

Often, these hurdles are simply the result of the “newness” of small business ownership and the loan process – if you haven’t been through these before, you may unknowingly miss key steps or be uncertain about how to move forward. With insight and help, you can avoid these issues and soon be on your way to the financing you need.

Pursuit can help

If you’re starting a business or are a seasoned business owner in New York, New Jersey, Pennsylvania, Connecticut, Illinois, or Delaware, and you’re considering applying for a small business loan, Pursuit can help.

Pursuit’s a leading small business lender offering loans and a line of credit for working capital, commercial real estate, equipment, and much more for a huge range of uses in most industries. From our first meeting, we’ll review the requirements for a startup business loan and help you get and stay on track throughout the loan process.

Contact Pursuit today!