While the U.S. Small Business Administration (SBA) has many different funding options available to help you grow your business, did you know that both the SBA 504 and SBA 7(a) loan programs can be used for commercial real estate? If you’re thinking about purchasing, renovating, or refinancing an existing commercial property, then it’s important to know which SBA loan best meets your needs.

Here’s a look at both options – the SBA 504 vs 7(a) – to help you understand what’s similar, what’s different, and which may be best for you.

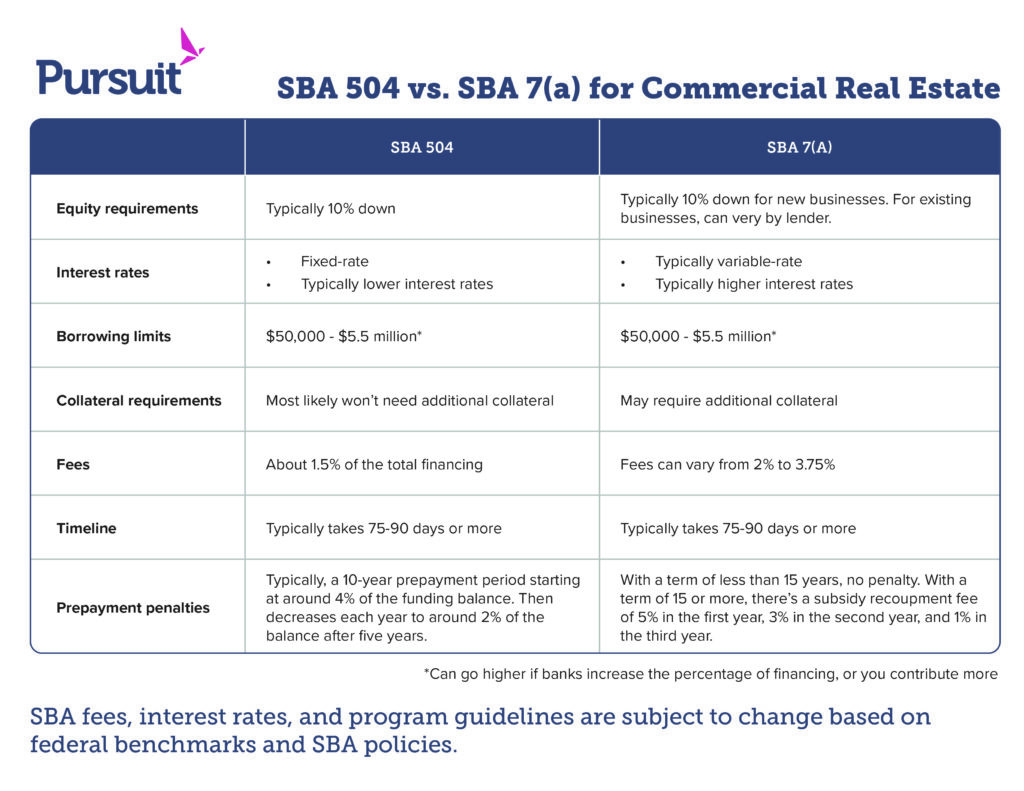

Which SBA loan is right for you?

Both the SBA 504 and SBA 7(a) loans can be great options for funding your commercial real estate. The right choice for your business mainly depends on how you plan to use the funds and how much flexibility you want in your financing.

In general, the SBA 504 loan is geared toward larger projects like purchasing significant equipment and owner-occupied commercial real estate, while the SBA 7(a) loan offers a broader use of funds.

Here’s a closer look at how each of the loan programs work:

SBA 504 loan for commercial real estate

The SBA 504 loan program provides long-term, fixed-rate financing for owner-occupied commercial real estate and heavy equipment or to refinance debt from these types of purchases. SBA 504 loans are always used together with a bank loan to finance up to 90% of total project costs. Here’s the typical SBA 504 loan breakdown:

- A bank funds 50% of the project costs with a conventional mortgage

- A Certified Development Company (CDC) funds up to 40% of the project costs

- You make as little as a 10% down payment on the project

Applying and getting approved for an SBA 504 loan has many similarities to the process of purchasing residential property, so if you’ve ever purchased a home through a bank, you’re already familiar with several of the steps.

However, commercial real estate projects are usually more complex than residential transactions, so extra steps may be needed. In addition, the SBA helps lenders provide loans to small business owners by offering loan guarantees for SBA loans, so a little extra documentation and due diligence are a part of the process.

SBA 7(a) for commercial real estate

The SBA 7(a) loan program offers funding for startups and growing businesses in any qualified industry. SBA 7(a) loans can be used for just about any business need, including commercial real estate projects. SBA 7(a) interest rates fluctuate, and the rate is determined by your financing needs.

As with SBA 504 loans, when SBA 7(a) loans are used for commercial real estate projects, the process will typically take a little longer than for an SBA 7(a) loan used for another purpose. However, it is still in line with the timeframe for conventional commercial real estate loans.

SBA 504 vs 7(a): Which is the better option for your real estate project?

Each loan option has its advantages, but the SBA 504 loan will usually be the most beneficial option for commercial real estate projects and purchases of heavy machinery or equipment. On the other hand, the SBA 7(a) loan is the SBA’s most popular product because of its flexible uses for things like inventory, working capital, equipment, and much more.

Here’s how they compare:

Equity requirements

Overall, the owner-equity requirement for real estate projects is one of the SBA’s major advantages over conventional loans (which typically requires 20-30% in owner equity).

- The SBA 504 typically requires a 10% payment in owner equity, although this may increase for some projects.

- The SBA 7(a) also usually requires 10% down in owner equity for new businesses, but for existing businesses, this can vary by project and at the lender’s discretion. Also, additional collateral is often required for projects at or around 90% financing.

Interest rates

On this point, the SBA 504 is typically more beneficial for commercial real estate purchases.

- The interest rate for an SBA 504 loan is fixed for the full term (10, 20, or 25 years) for the SBA 504 portion of the financing, which makes payments predictable over the life of the loan. Additionally, SBA 504 loan interest rates are typically less than the interest rates for SBA 7(a) loans or even below market rates for traditional lenders.

- SBA 7(a) loans are usually variable-rate loans, meaning that your payment amount will likely vary over the life of the loan. However, the rate can be fixed at the lender’s discretion. In addition, the interest rates on SBA 7(a) loans may be higher than those for conventional commercial real estate loans.

Maximum borrowing limits

SBA 504 loans are available from $50,000 to $5.5 million. For larger projects, banks can increase the percentage of financing, or you can put in more than 10% equity. For example, if a project total is $30 million, the breakdown could look like this:

- SBA 504 financing: $5.5 million

- Owner equity of 15%: $4.5 million

- Bank financing: $20 million

While projects of this size aren’t common, they’re certainly possible.

- SBA 7(a) loans range from $50,000 to $5 million, with lenders funding up to 100% of the project cost. Since there’s no additional bank partner, if a project surpasses this option’s maximum SBA contribution of $5 million, any additional funding needed would have to come from owner equity.

For example, if a project’s total cost was $7.5 million, then the SBA 7(a) loan could cover the first $5 million, and your contribution would have to cover the rest.

Collateral requirements

- In most cases, the SBA 504 program only takes liens on the fixed assets that are financed through the loan.

- For the SBA 7(a) program, when the financed assets aren’t enough to secure the loan, you may be required to put up additional collateral.

Fees

- SBA 504 loan fees are generally about 3% of the SBA 504 portion of the loan or about 1.5% of the total financing package.

- SBA 7(a) loan fees are applied to the guaranteed portion of the total financing package and can run from 2% to 3.75%.

Length of time from application to approval

SBA 504 and SBA 7(a) loans are comparable to each other and the length of time it takes for the real-estate loan approval and closing process with conventional commercial loans.

However, because the SBA loan application is typically submitted after the initial lender application, it can seem like the SBA loan-approval process takes longer. For commercial real estate transactions, it’s common for approval timelines to extend due to environmental reviews, real estate appraisals, special permits, or for SBA 7(a) loans, appraising personal property that’s pledged as collateral. Typically, it takes about 75-90 days or more.

Prepayment penalties

The SBA may charge a prepayment penalty if your loan is paid off before the end of its term.

- For SBA 504 loans, the prepayment penalty period is typically 10 years and currently starts at around 5% of the SBA 504 balance of financing; currently, this amount decreases each year to around 2% of the SBA 504 balance of financing after five years.

However, it’s important to know that fees vary over time because they’re based on fluctuating federal interest-rate benchmarks. For example, if the rates are low now, prepayment fees are low. With an increase in interest rates, the prepayment penalty fee rates are likely to increase. - SBA 7(a) loans with terms under 15 years have no prepayment penalty. Loan terms above 15 years require a “subsidy recoupment fee” of 5% in the first year, 3% in the second year, and 1% in the third year.

What else should you know when you meet with lenders?

Here are three key points to keep in mind when you meet with lenders about your commercial real estate financing needs:

1. Ask your lender questions

Many lenders offer SBA 7(a) loan options on their own, but to provide SBA 504 loans, a bank needs to partner with a CDC. Because of this, sometimes lenders won’t be familiar with the SBA 504 loan program or know of local CDC partners, so they may not offer the SBA 504, even if it’s the best option for your project.

For that reason, when you talk to lenders, be sure to ask if they know about the SBA 504 option and ask to hear about it if the lender doesn’t offer it upfront. You’re advocating for your right to the best term for your commercial real estate loan, so find a lending partner who will work to get them for you.

2. Be prepared before you meet with lenders

When you meet with lenders, have as much information about your project as possible, including cost estimates or sale prices for property. Lenders need this information before they can tell you what the cost structure could be, including the equity requirement and potential collateral.

3. Be realistic about your project timeframe

It’s a common misconception that SBA loans can take a while to be approved and to close. In reality, SBA transactions are thorough, but they’re not complicated. Like any real estate transaction, the first time is always daunting. But, if you provide your SBA lender with a complete and accurate application and financial picture, your lender should be able to deliver a loan decision within a timeframe that’s comparable to a conventional bank loan.

SBA 504 vs 7(a): Pursuit offers both, so talk to us today!

SBA 504 and SBA 7(a) loans are great options for small businesses, but there are important differences between the two when it comes to commercial real estate projects. Working with a lender familiar with both SBA 504 and SBA 7(a) structures can help ensure that you get the funding that best meets your business’s needs.

If you’re considering SBA financing for your business’s commercial real estate project, speak to an SBA lending expert today!

We offer both of these SBA loans and more funding options for businesses located in Connecticut, New York, New Jersey, Pennsylvania, Illinois, and Delaware, and we’ll help you through the entire process.