As a small business owner, one thing you’ll always need is working capital. These are the funds needed to cover day-to-day and shorter-term operational expenses. Whether you’re a start-up that’s ready to launch and grow, an existing business that’s positioned for expansion, or a seasonal business getting ready for a slowdown, working capital is essential. A business working capital loan can help whenever you need to bridge the gap.

In this overview, you’ll learn how to determine your working capital needs and what your options are for a small business working capital loan.

Key considerations for a working capital loan

There are two key points you’ll need to consider when looking for working capital loans:

- Using the right type of funding: If you use a short-term loan to fund longer-term expenses (like salaries, rent, utilities) for expansion or startup operations, you can strain your cash flow because repayment may be due before you see an increase in revenue and profits.

- Getting sufficient funding: You may experience a financial pinch if you don’t secure enough working capital to support your business during its startup or growth phase. If you overestimate revenue or underestimate expenses, you’ll find yourself short of funds. When you’re short on working capital, you may miss out on new opportunities, incur late payments to vendors and creditors, and damage your credit score.

Understanding these considerations sets the foundation for determining how much working capital your business needs, and the best ways to access it.

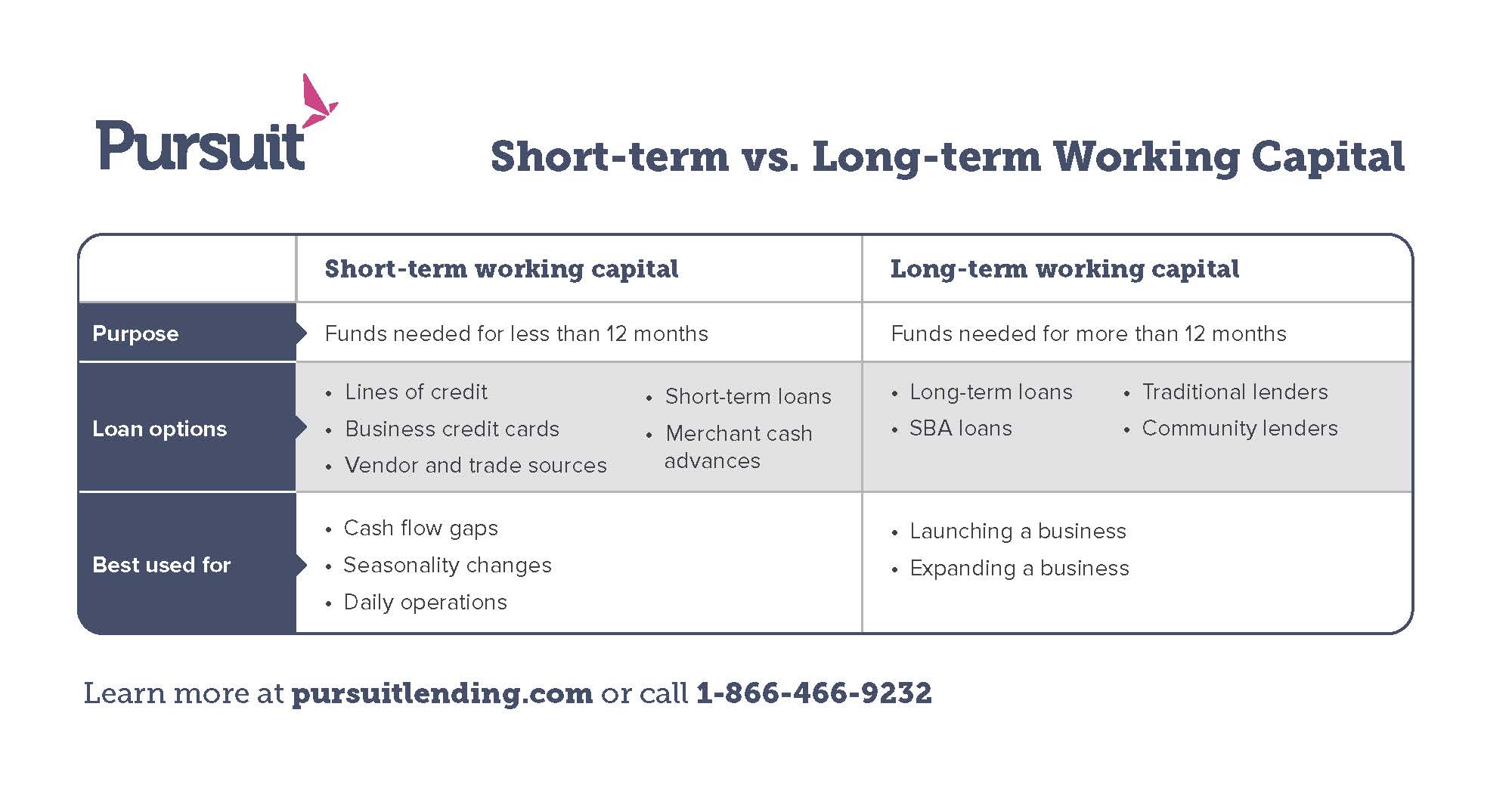

How much working capital does your business need?

The first step to getting enough working capital is to figure out how much business financing you need and how long you need it. This will help you and potential lenders determine which type of working capital loan best suits your needs.

Short-term working capital needs

Short-term working capital needs are usually needed for less than 12 months. These needs frequently result from business seasonality, like purchasing inventory for peak selling seasons, or from fulfilling new contracts, such as purchasing materials or equipment or adding staff. While you’re waiting for payments on the contracts or pending accounts receivable, your working capital needs may grow.

Short-term working capital needs are best served by short-term loan products such as lines of credit. Business lines of credit provide a maximum amount of borrowing for a set period (12 months) based on your business’s inventory and receivables. Funds can be drawn down and repaid throughout the commitment period, and you can pay interest only monthly. Your lender typically requires the principal to be repaid in full at least annually.

Long-term working capital needs

Working capital needs lasting more than 12 months are common for start-ups or for expanding existing businesses. Start-ups need working capital to hire staff, for professional fees and filings, and anything else to get the business up and running. If your business is a start-up, it’s a good idea to have at least six to 12 months of operating expenses available (ideally 12 to 18 months). This ensures that you’ll have enough funds available as business operations start, and before your business becomes profitable.

If you have an existing business, you should have enough funds to cover at least three to six months of operating expenses to address slow periods. If you’re expanding your business, you might have working capital needs similar to start-ups, as you add staff, increase inventory, and face other growing overhead expenses.

Longer-term working capital needs are best met by term loans with longer repayment periods of three years or more. A typical term loan for working capital can range from three to seven years depending on the lender. You’ll make monthly payments of both principal and interest over the term of the loan.

What working capital loans are available for small businesses?

There are several sources of working capital available to your small business. Business working capital loans can vary based on your number of years in business, your creditworthiness, industry, and other factors.

It’s important to note that there are business working capital loan options that specifically support start-ups, underserved communities, and more.

1. Vendor and trade sources

The most common sources of short-term working capital for inventory purchases are the credit terms offered by vendors. If your business is a start-up, this may be difficult to negotiate, as vendors may require cash-on-delivery (COD). Once you’ve established vendor relationships, try negotiating payment terms of 15 to 30 days, which gives you time to turn over inventory and have more cash on-hand.

If you need money to make equipment purchases, try to find vendors who offer financing programs. While the interest rates might be higher than traditional bank financing, this can still be a good option. Be sure to do your homework to ensure you’re getting a good deal.

If you have accounts receivable, you may be able to reduce ongoing working capital needs by offering early-payment discounts to customers who meet the terms that you set. For example, if your customer pays you in 10 days they’ll receive a 2% savings, while you receive your money in 10 days rather than 30. Although you’re offering a discount, having cash available sooner can be lower than the cost of borrowing against a line of credit.

2. Working capital loans from traditional lenders

Commercial banks and credit unions offer the most affordable working capital loans if your business qualifies. Develop a relationship with a loan officer at the bank that has your commercial account. Loan officers can advise you on what’s available and your likelihood of approval. Even if you only receive a small line of credit or loan to start, you’ll build your business credit history and add to your available cash flow.

Traditional lenders can be hesitant to finance businesses with less than two years of operations, though, so start-ups are less likely to get approved early on. Still, it’s worth it to establish a relationship with your commercial bank officer so they can provide financing advice to you down the line.

Another way you can leverage your bank relationships to improve working capital is through overdraft agreements. Like loans and lines of credit, these agreements are negotiated in advance. Once in place, they allow your business to essentially “borrow” amounts as needed, without penalty, though there will likely be an interest expense.

3. Working capital loans from community lenders

Small Business Administration (SBA)-backed lenders and alternative community lenders, like Community Development Financial Institutions (CDFIs), are also great sources of working capital for small businesses. These lenders can help business owners:

- In the start-up or early phases with little financial history

- With less-than-perfect credit

- In riskier industries like restaurants or retail

- With limited or no collateral

- In underserved communities

SBA loans aren’t actually made by the SBA; instead, the SBA provides loan guarantees to traditional lenders and other funders, such as CDFIs, to encourage lending and support small businesses. The SBA offers many loan programs that can meet your working capital needs.

CDFIs are non-profit, mission-driven organizations that typically offer loans to business owners who need more flexible terms and financing options. They provide small business owners with manageable payments to keep more working capital on-hand for growth and are great educational resources, especially for early-phase expanding businesses.

4. Alternative lenders and merchant cash advance services:

There are other financing options for working capital that can appear attractive to small business owners but that should be approached with extreme caution, if at all. Predatory online lenders who base lending decisions on incoming merchant receipts and daily bank deposits may seem too good to be true, and more often than not will cost your business more money in the long run.

While these lenders offer quick and easy applications and access to fast cash, the money comes with extreme interest rates. They often include annual percentage rates (APRs) of 50% or more. They can also have rapid repayment terms, often requiring daily withdrawals from your bank account. Before long, most small business owners find these terms burdensome, putting their business at risk.

Remember, never fund a longer-term working capital need with one of these rapid-repayment loan products!

Pursuit can guide you through your working capital needs and more

If your business could use a working capital boost, or other business funding need, Pursuit has you covered! Every day, we support small business owners in New York, New Jersey, Connecticut, Pennsylvania, Illinois, and Delaware through a range of tailored and beneficial loans.

Contact us today to learn more about how we can help you!