Are you a small business owner looking to grow your business? Are you trying to figure out how much money you’ll need to put a growth plan into action? One of the key questions you should ask yourself is, “how much working capital do I need to grow my business?” This article will help answer that question.

What is working capital?

Working capital is the total amount of capital you’ve invested in running your business. This is the money your business has available to meet your short-term (and sometimes long-term) obligations. The basic equation for working capital is:

Working capital = current assets – current liabilities

Current assets are short-term and can be converted quickly to cash. This includes your accounts receivable and inventory. Current liabilities are obligations that will be due within one year, which are primarily your accounts payable and short-term debt

The term “working capital” is often misused when discussing a business’s financing needs, especially for startups. For example, if your business is looking to get funding for an advertising budget and salaries for new employees, what you need is long-term capital or equity. If your business is unable to support the expenses for advertising and salaries, then most likely it is undercapitalized. If your business is projecting losses in its first year, you most likely need equity, and not working capital.

How much working capital is needed to grow your small business?

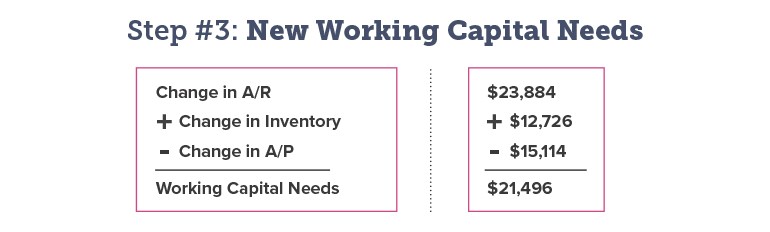

To grow your business, the amount of working capital you need is:

New working capital needs = Change in accounts receivable + Change in inventory – Change in accounts payable

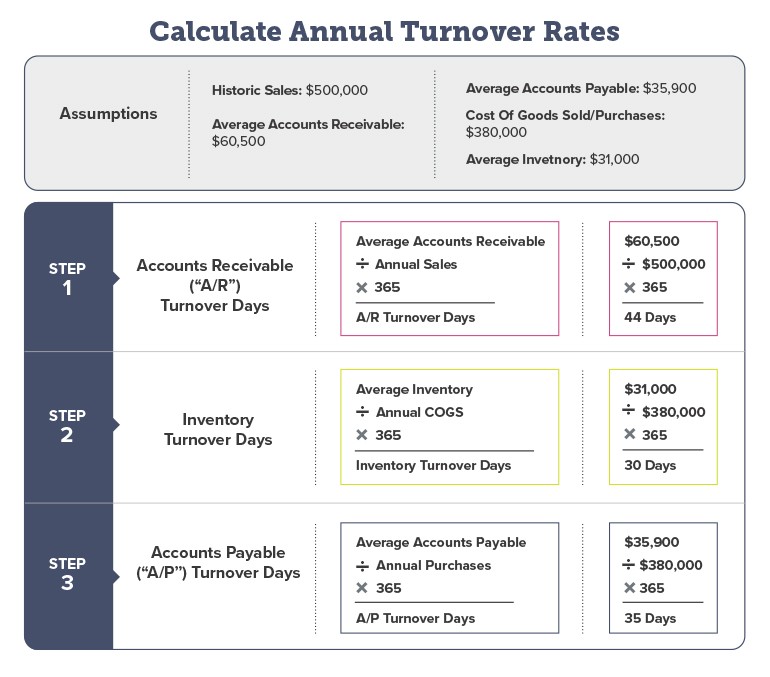

However, before you calculate, you need to calculate your turnover rates. And to do that, you need to understand the working capital cycle – how money flows through your business, including how quickly current assets are turned into cash and how quickly that cash is used to pay current liabilities. The working capital cycle is also referred to as your turnover rates for accounts receivables, inventory, and accounts payable.

How to calculate your turnover rates

Your business’s historical turnover rates are the first step in forecasting your growing working capital needs. You need to analyze your actual income statement and balance sheet to find out the following information:

- How many days of inventory do you keep on hand (inventory turnover)?

- How many days does it take for customers to pay you (accounts receivable turnover)?

- How many days do you take to pay your vendors (accounts payable turnover)?

Here’s how to calculate your annual turnover ratios:

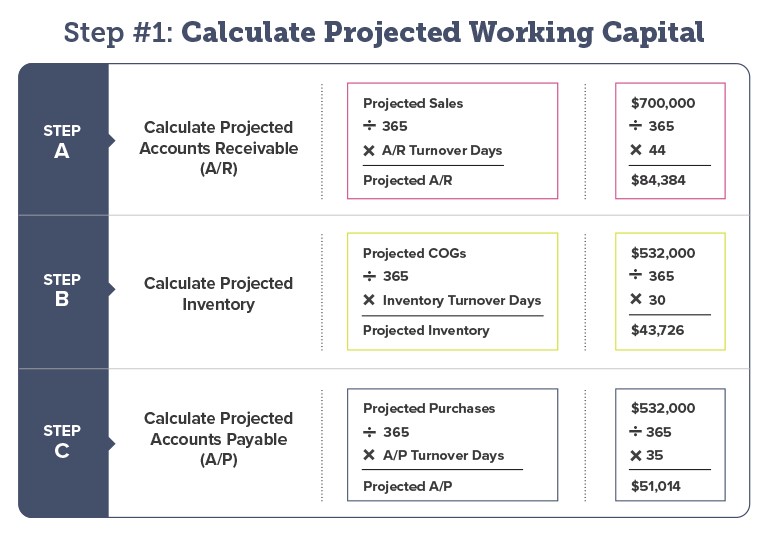

Now that you calculated your turnover rates, you’re ready to forecast your working capital needs based on your plan for growth. This growth will require carrying higher levels of inventory and accounts receivable, which will require additional working capital financing. But “How Much?” is the question.

To do that calculation, you need to have a projected income statement, which includes both projected sales and cost of goods sold. Using these figures and the working capital turnover ratios shown above, you can get an estimate of how much additional working capital is needed to grow your business. Here’s an example to show how.

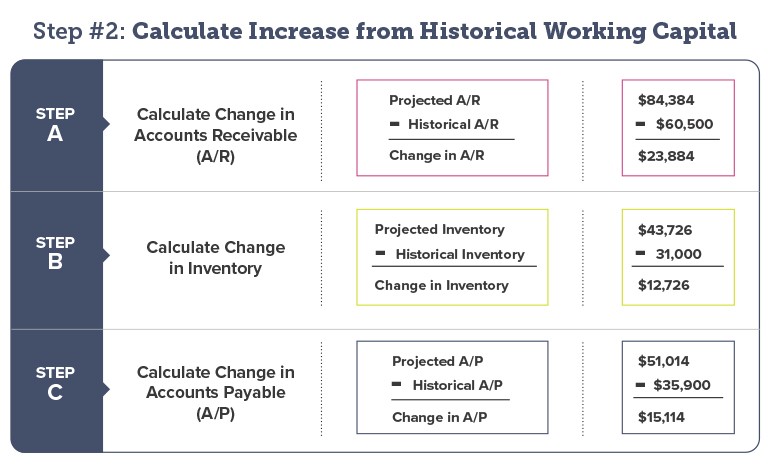

Using these projected balances, you can figure out the changes to working capital by calculating the difference between your projected and historical balances for accounts receivable, inventory, and accounts payable.

So what does this all mean? Your new working capital needs equals the change in Accounts Receivable plus Inventory minus Accounts Payable.

In this example, if you project to grow your sales from $500,000 to $700,000, you’ll need additional working capital of $21,496.

How to fund your working capital needs

For small businesses that have been in operation and generating profits, you’ll most likely have reinvested some of the profits back into the business (retained earnings). You reinvest your profits into your inventory, use the profits to carry increased levels of receivables, or you use the profits to pay down your trade suppliers. As a result, retaining these profits increases your working capital, allowing you to grow.

If you didn’t earn or retain sufficient profits to finance your own growth, you may need to turn to borrowing money for your increased working capital needs. However, small businesses find it difficult to gain working capital financing from traditional banking sources.

As a result, you may be tempted to turn to predatory lenders who offer quick and easy access to funding. These lenders often offer high interest rates, high fees, and difficult terms. Before you agree, it’s a good idea to calculate the annual percentage rate (APR) of a merchant cash advance, and a typical online loan to uncover the true cost of the loan.

What are alternative sources of working capital financing?

There are many responsible, community lenders available to help you fund your working capital needs. For example, Community Development Financial Institutions (CDFIs) are nonprofit, private financial institutions that provide affordable lending to small business owners who may not qualify for traditional financing.

In addition to their own loan programs, many CDFIs also participate in U.S. Small Business Administration (SBA) loan programs, which offer significantly lower APRs than other non-banking sources of financing.

Talk to Pursuit about your working capital needs

When growing your small business, you’ll need to invest in your inventory and accounts receivable, and have sufficient working capital.

If your business could use a working capital boost, or other business funding need, Pursuit has you covered! Every day, we support small business owners in New York, New Jersey, Connecticut, Pennsylvania, Illinois, and Delaware through a range of tailored and beneficial loans.

Contact us today to learn more about the ways we can help you!