When you look at your business’s performance, you’re often looking at the cash coming in and out to see how it’s doing? The problem with that is you’re only looking at part of the picture. To effectively manage and grow your business, you’ll need to look at what’s happening now and what’s on the horizon. To do that, you’ll need to understand your business’s accounts payable and receivable.

What are accounts payable and receivable?

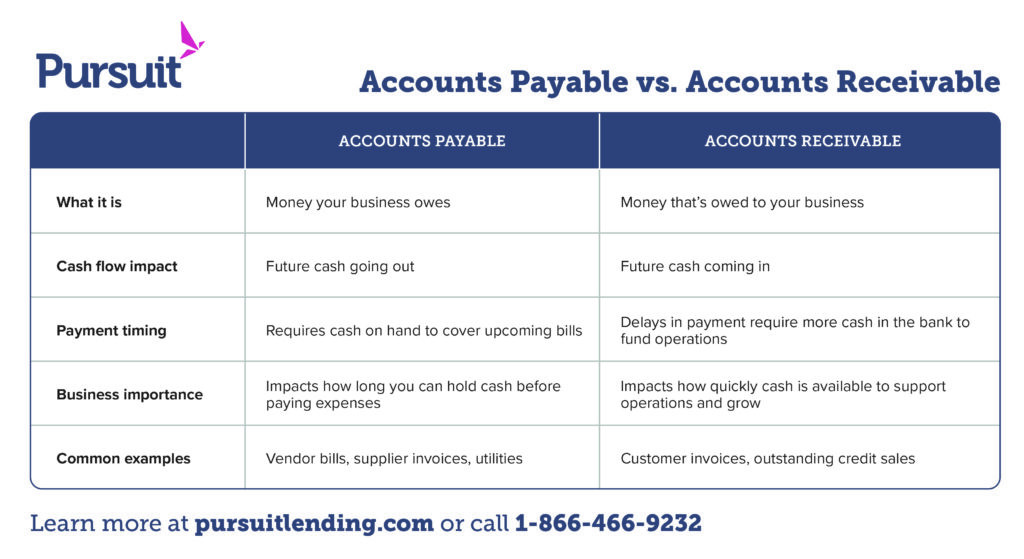

Your accounts payable (AP) are bills for services that your business has already used or goods that your business has already received. If you have a $1,000 in accounts payable, you’ll need to spend $1,000 in the very near future to pay off those bills. Your accounts receivable (AR) are invoices that your business has issued that haven’t been partially or completely paid. Your AR is money that’s owed to you.

Not all businesses have the same experiences with accounts payable and receivable. Here are some examples to explain:

- If you run a restaurant, you’ll likely have little to no AR or AP. You pay for your food product when it’s delivered and charge your customers for their meals before they leave.

- If you run a construction business, you’ll likely have a lot of AR and AP because your customers usually take a month or more to pay off their invoices, and you may use subcontractors, who typically don’t pay for several weeks.

Accounts payable and receivable are important for your business’s future cash flow. If you’re operating your business on a cash basis, your receivables are the cash that will be coming in, and your payables are the cash that will be going out.

The longer it takes for your receivables to come in, the more cash in the bank you’ll need to fund your operating expenses in the meantime. The longer you take to pay your payables, the more cash you’ll have in hand to continue funding your operation.

How to manage your accounts receivable?

Here are the top strategies to organize and streamline your accounts receivable:

1. Decide when to offer credit

A strong accounts receivable strategy starts with deciding when – and whether – you can offer credit to your customers. Before making this part of your business, you should ask yourself:

- Can you ask your customers to pay upfront?

- If not, can you ask them to pay a large deposit upfront?

You can often find the answers to these questions by looking at what the best practices are for your industry, but don’t be afraid to push the boundaries of those norms. Any money you receive from your customers sooner rather than later will benefit your business’s cash flow.

2. Make your payment terms strict

Setting clear boundaries and deadlines is very important when it comes to customer credit. You can start by:

- Setting your invoices to be “due upon receipt,” meaning due immediately

- Establishing a clear penalty for payments that haven’t been made in 30 days (such as accrued interest or a flat fee)

When these terms are laid out from the start of a relationship with a new customer, it creates a strong incentive for them to pay on time. If they violate your payment terms, stop offering credit to the customer, and immediately stop all work for them until they settle their outstanding balance.

3. Ask your customers to pay you

When it’s time for you to ask your customers to pay you, the business relationship becomes serious, with a dynamic of mutual respect and cooperation. There’s never a “right” time to ask your client to pay you, but it’s a good idea to:

- Invoice your customers immediately after giving them their products or services, or exactly on the date you said you would invoice them

- Send your customers reminders to pay you if they’re late, and even informing them of your dissatisfaction, is important as well

Your relationship with your customers should be equal. You give them goods and services on a timely basis, and they must pay you on a timely basis.

Good invoicing platforms have tracking capabilities, and you’ll likely find this capability in your bookkeepingprogram. This means that you can see when your customers received their invoice via email, and each time they view the invoice. These tools give you more footing in a discussion with your customers about settling their outstanding balances and make assigning payments to the right invoice foolproof.

4. Set up credit policies

As your business grows, it helps to set up rules and guidelines for offering credit to your customers. This should start when you onboard a new customer:

- Research your customer by reviewing their Dun and Bradstreet report (if available) to see outstanding payment obligations and payment history. Ask for recommendation letters, and for larger contracts, consider requesting their financial statements as well.

- For services, put payment terms in a clear section of your engagement letter and break down each part of your overall scope of work, invoice timing, and late payment penalties. For products, provide customers with your terms before selling them.

- Require your customers to pay immediately for the first year, then offer them up to 30 days of credit. This allows you to assess payment behavior across busy and slow seasons and limit credit for customers who consistently pay late.

A system like this can be difficult to implement, especially if you have very large customers that account for a large share of your sales. These customers will try to bend the rules because they know you depend on their sales. You can lower the risk of this by building a diverse customer base that evenly contribute to your business’s income.

How to manage your accounts payable

Here are the top strategies to organize and streamline your accounts payable:

1. Build vendor relationships

Your vendors are businesses with many of the same cash flow concerns that you have. It might seem enticing to stretch out your payments, but that can be short-sighted.

Building a relationship with your vendors means paying on their terms. Once you build a reliable history of on-time payments, then you can negotiate a payment term that is fair for them and you.

2. Use your bookkeeping software’s tools

All good bookkeeping software includes a module for bill management. Use these tools to their full extent! If you enter every bill you receive into the bill manager, you’ll never miss a payment.

You’ll also get alerts for upcoming bills, plus you can even pay your bills and have checks printed automatically. Using these tools will make the financial statements generated by your bookkeeping software more accurate and provide you with more insight into your business.

3. Communicate payment problems

At some point, you may need to tell your vendors that you’re not going to be able to meet their payment deadlines. Mastering this conversation is key to coming out of these situations with vendor relationships intact. Be candid about your situation. Reach out to your vendors proactively – ideally before the deadline.

There are some steps you can take to avoid this scenario in the first place. One way is having a higher-cost credit card that you can use only as an emergency if you think your cash flow will have a gap this month. Another strategy is to secure a line of credit. These generally carry a lower interest rate than credit cards and allow you to carry a balance until your accounts receivables are paid.

Need working capital to cover your cash flow gaps? Reach out to Pursuit

Having a good understanding of your receivables and payables is critical to your business’s cash flow. By following these tips, you’ll be able to have a clear picture of what you owe and what’s owed to you at any given moment, and be able to proactively handle any cash flow issues.

If you need some extra working capital to cover your cash flow gaps before your receivables are paid, reach out to Pursuit. With more than 15 different loan products and a line of credit, we can help you couver your funding needs so you can keep your business moving forward.