Small business risk assessment isn’t something you’re likely to think about as you launch and grow your business, but it’s essential to your long-term success. In this article, you’ll learn the steps you need to take to ensure that your business is better prepared to weather a range of risks and emerge financially and operationally strong.

How to assess and address risks for your business

Here are the steps to take to identify and address challenges and opportunities:

Step 1: Examine your business operations

Look at all your key internal and external business operations and ask yourself, “What would happen if this were suddenly unavailable, temporarily or permanently?” Make sure to take notes as you go through this list, so you can be ready for the next step.

Management

Who runs your business? If yours is a solo operation, think about what would happen if you weren’t available. Make sure you have a succession plan to pass the business on to a family member or to sell it. If you have partners, decide what would happen if one (or more) left the business and how it would impact operations. What about your financials, including any outstanding business debt? Work with your business’s legal advisor and accountant on succession and contingency plans.

Staff

It’s a good idea to examine which staff roles are essential to business operations. If you haven’t taken that step yet, do so now. Also, figure out why those roles are essential, so that you can identify the key skills and qualities you need if an essential employee has to be replaced. Spend some time gauging your staff’s morale. Nothing drags down productivity like unhappy employees. Get their input on ways to improve or accommodate their preferences.

Vendors and suppliers

List out where and how you get the essential supplies you need to run your business. What would you do if key suppliers couldn’t get the materials or products you needed? It’s important to consider the following questions:

- If your business is a priority to them, and if not, how can you improve your standing? There are several ways, such as ordering in line with their manufacturing schedules or renegotiating payment terms.

- Are your vendors financially stable, so that they can weather challenges?

- Do you have backup suppliers available? If not, what would it take to establish those inventory lifelines?

- Could you pivot your products or services to generate income, independent of vendor issues?

IT infrastructure and cybersecurity

Most small businesses have expanded online services and are increasingly targeted by ransomware and hacking schemes. Ensure your IT infrastructure is protected and your customer information is secure. If you’re not sure, it’s a worthwhile investment to have an expert review your IT programs.

Real estate and equipment

Whether you own or lease, ensure that you have ample insurance coverage for a range of potential natural and manmade disasters. Review your policies with your insurer for coverage if something happens to an adjacent property. While it’s essential that the tangible items are covered — like real estate and equipment — find out if coverage is available for financial losses from business disruptions.

Finances

Stress-test your budget by running your numbers with a 10% increase in revenue and expenses and with a 25% decrease in revenue and expenses. Determine what changes you would have to make to leverage opportunities or kick into survival mode. If you haven’t already, check to see if you have an effective business budget.

Always have sufficient working capital and know your financial safety nets. Get a loan or a line of credit if you’re operating too close for comfort, to allow you to survive through disasters, or to leverage new opportunities that arise, such as when a competitor decides to close or sell.

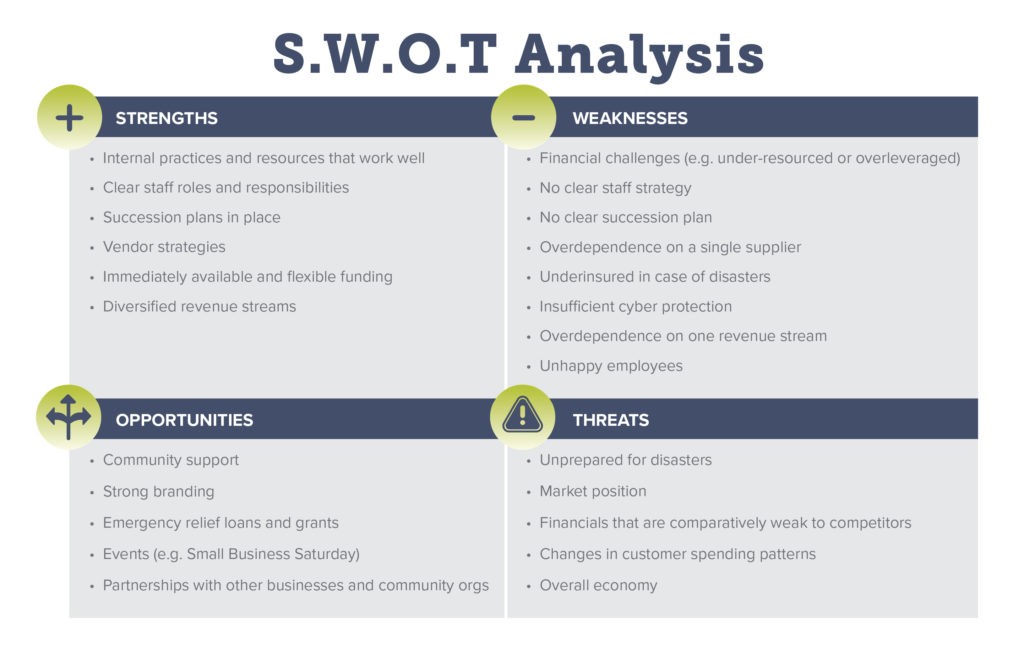

Step 2: Create a SWOT analysis for risk management

A SWOT analysis is a commonly used business tool that helps you identify strengths (S), weaknesses (W), opportunities (O) and threats (T). The strengths and weaknesses are usually internal assets and challenges, while the opportunities and threats are externally driven.

You can use the sample layout below as a template. Download your own S.W.O.T. analysis template here. With the notes you made in Step 1, fill in the assets and challenges that you identified.

Step 3: Take action to mitigate risks

Highlight the major challenges and identify the actions needed to reduce the risks you identified. For example, if your SWOT analysis shows that your business isn’t sufficiently insured, contact your insurance agent immediately. Or, if you don’t have sufficient working capital to get you through another season, start exploring your funding options.

If you need working capital or other funding, Pursuit can help

If your risk assessment indicates that you need more working capital or another funding need, contact us today.

Pursuit offers access to more than 15 loan programs to business owners in New York, New Jersey, Pennsylvania, Connecticut, Illinois, and Delaware. We also offer insightful resources and business advisory services to help your small business get stronger today and thrive tomorrow.